Simulation task: recovering causal effects from post-treatment selection induced by missing outcome data

selection bias

mediation

regression

IPW

doubly-robust

TMLE

A simulation exercise on missing data, selection bias, causal inference and TMLE

Published

October 15, 2023

Objective

The goal is to estimate the average treatment effect (ATE) of a binary treatment on a continuous outcome, from observational data where the outcome is subject to a missingness/selection mechanism.

For this task, we employ:

The structural causal models (SCM) framework (Pearl 2009)

A generated observational dataset

A backdoor admissible set

A missing-outcome mechanism that allows recoverability via IPW and regression adjustment

Generated data from substantive model and missingness mechanism

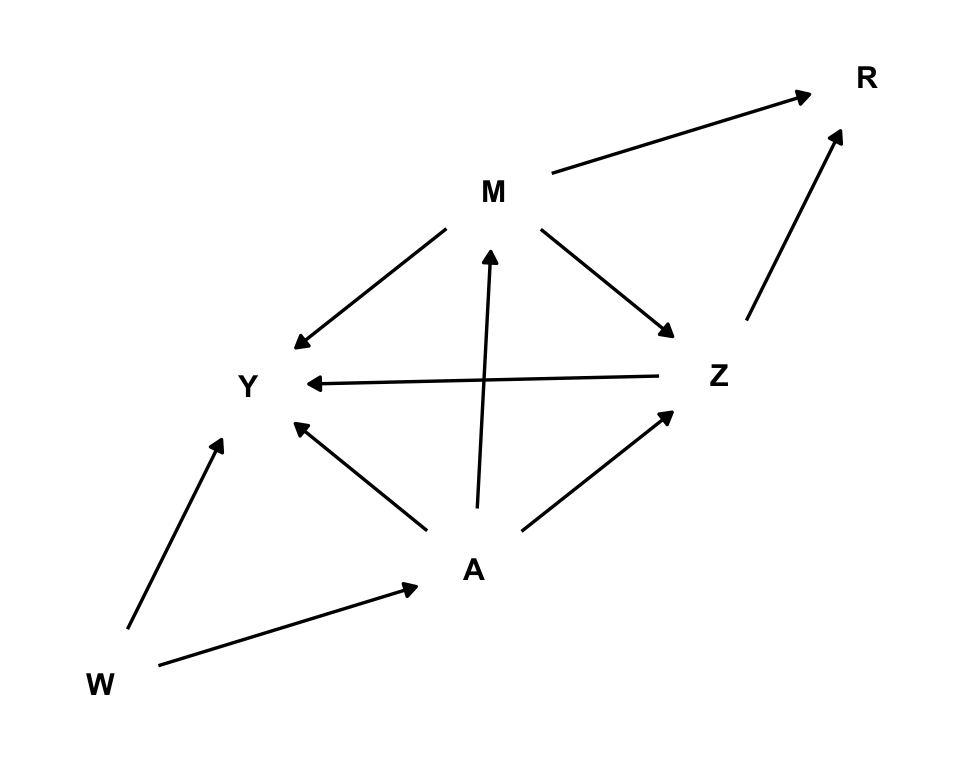

We build a directed acyclic graph (DAG) \(\mathcal{G}\), involving the exposure \(A\), the outcome \(Y\), a confounder variable \(W\), mediators of the effect \(M,Z\), and missingness mechanism for the outcome \(R\)

Code

# DAG visualizationlibrary(ggplot2)library(dagitty)library(ggdag)dagify( A ~ W, M ~ A, Z ~ A + M, Y ~ W + A + M + Z, R ~ M + Z) %>%tidy_dagitty(layout ="kk") %>%ggplot(aes(x = x, y = y, xend = xend, yend = yend)) +geom_dag_point(color='white',size=0.5) +geom_dag_edges() +geom_dag_text(color='black') +theme_dag()

A fixed set of causal mechanisms \({f}_V:\text{supp}\, \text{pa}(V;\mathcal{G})\times \text{supp}\, U_V\rightarrow\text{supp}\, V\) allows us to generate fake data from seeds (noises and exogenous variables) in a controlled environment, along with all necessary counterfactual variables.

Generated substantive variables are:

\(W\in\mathbb{R}\) = confounder

\(A\in\{0,1\}\) = binary treatment

\(Y\in\mathbb{R}\) = outcome

\(M,Z\in\mathbb{R}\) = mediators of the effect of treatment on the outcome

Counterfactual variables are:

\(M^A,Z^A\) = value of mediators \(M,Z\)had the individual taken treatment\(A\)

\(Y^{A}\) = value of the outcome had the individual taken treatment\(A\)

We employ the following nonlinear specifications for the causal mechanisms: \[

\begin{aligned}

W &= U_W \quad & U_W\sim N(0,1)\\

A &= \mathbb{I}[0.9W -0.09\,\text{sign}(W)\,W^2 + U_A > 0],\quad & U_A\sim N(0,1)\\

M &= -0.50 + A + U_M,\quad & U_M\sim N(0,1)\\

Z &= 0.12\,[4.2 + 0.25\,(2A-1) + 0.30M + 0.05\,(2A-1)\, M + U_Z]^2,\quad & U_Z\sim N(0,1)\\

Y &= 1.80W+ 0.20W^3 + 0.75\,(2A-1) + 0.50\,(2A-1)\, W & \\

&\qquad + 2.00M + 0.50\,(2A-1)\, M + 0.80\,(2A-1)\, Z+ U_Y,\quad & U_Y\sim N(0,11)\\

\end{aligned}

\]

Missingness mechanism

We run the analysis under four different scenarios: combining three missingness mechanism of the outcome, and scenarios of no misspecification, and misspecification on the propensity score, on \(Q_1\), and on \(Q_2\) + probability of selection. Selection mechanisms share a simple probit specification on the mediators \(M,Z\):

\[

R = \mathbb{I}[\theta + 0.29 M + 0.54 Z + U_R > 0],\quad U_R\sim N(0,1)

\]

Different configurations of \(\theta\) generate missingness mechanisms of different strength.

Case 1: severe selection: by setting \(\theta=-1.20\), we obtain around 50% of missing cases

Case 2: medium selection: by setting \(\theta=-0.35\), we obtain around 25% of missing cases

Case 3: low selection: by setting \(\theta=0.40\), we obtain around 10% of missing cases

A dataset (full.data) of \(N=10\,000\) samples was generated:

Code

# Causal mechanisms ------------------------------------------------------------# Causal mechanism for treatment assignmentcoef.A =c(0.00, 0.90, -0.09)fun.A =function(w, u){ dat =as.numeric(c(1, w, sign(w)*w^2)) lo =dot(coef.A, dat) + ureturn(as.numeric(lo>0))}# Causal mechanism for mediator 1coef.M =c(-0.50, 1.00)fun.M =function(a, u){ dat =as.numeric(c(1, a)) li =dot(coef.M, dat) + ureturn(li)}# Causal mechanism for mediator 2coef.Z =c(4.20, 0.25, 0.30, 0.05)fun.Z =function(a, m, u){ dat =as.numeric(c(1, 2*a-1, m, (2*a-1)*m)) li =0.12*(dot(coef.Z, dat) + u)^2return(li)}# Causal mechanism for outcomecoef.Y =c(0.00, 1.80, 0.20, 0.75, 0.50, 2.00, 0.50, 0.80)fun.Y =function(w, a, m, z, u){ dat =as.numeric(c(1, w, w^3, 2*a-1, (2*a-1)*w, m, (2*a-1)*m, (2*a-1)*z)) li =dot(coef.Y, dat) + ureturn(li)}# Causal mechanism for missingness mechanisms. Rcoef.R =c(0.29, 0.54) fun.R =function(m, z, u){ dat =as.numeric(c(m, z)) lo = r.bias +dot(coef.R, dat) + ureturn(as.numeric(lo>0))}# Generate the data ------------------------------------------------------------# Number of samplesN =1e4# Seed set.seed(77)# Generate exogenous variables: independent confounders and noises, # plus fixed treatment assignments A.1 and A.0full.data =data.table(noise.A =rnorm(N, 0, 1),noise.M =rnorm(N, 0, 1),noise.Z =rnorm(N, 0, 1),noise.Y =rnorm(N, 0, 11),noise.R1 =rnorm(N, 0, 1),noise.R2 =rnorm(N, 0, 1),noise.R3 =rnorm(N, 0, 1),W =rnorm(N, 0, 1),A.1 =1, A.0 =0)# Generate observationsfull.data = full.data[, A:=mapply(fun.A, W, noise.A)] %>% .[, M:=mapply(fun.M, A, noise.M)] %>% .[, M.1:=mapply(fun.M, A.1, noise.M)] %>% .[, M.0:=mapply(fun.M, A.0, noise.M)] %>% .[, Z:=mapply(fun.Z, A, M, noise.Z)] %>% .[, Z.1:=mapply(fun.Z, A.1, M.1, noise.Z)] %>% .[, Z.0:=mapply(fun.Z, A.0, M.0, noise.Z)] %>% .[, Y:=mapply(fun.Y, W, A, M, Z, noise.Y)] %>% .[, Y.1:=mapply(fun.Y, W, A.1, M.1, Z.1, noise.Y)] %>% .[, Y.0:=mapply(fun.Y, W, A.0, M.0, Z.0, noise.Y)] %>% .[, ITE:=Y.1-Y.0] # Generate missingness indicator, case 1: R1r.bias =-1.20full.data = full.data[, R1:=mapply(fun.R, M, Z, noise.R1)]# Generate missingness indicator, case 2: R2r.bias =-0.35full.data = full.data[, R2:=mapply(fun.R, M, Z, noise.R2)]# Generate missingness indicator, case 2: R3 y R4r.bias =0.40full.data = full.data[, R3:=mapply(fun.R, M, Z, noise.R3)]# A glimpse of the datafull.data[,8:24] %>%head() %>%kable(caption ="Table 1: A glimpse at the generated data")

Table 1: A glimpse at the generated data

W

A.1

A.0

A

M

M.1

M.0

Z

Z.1

Z.0

Y

Y.1

Y.0

ITE

R1

R2

R3

0.6598987

1

0

1

-1.1125637

-1.1125637

-2.1125637

2.862417

2.862417

2.1626663

-9.889348

-9.889348

-16.45675

6.567402

1

1

1

-0.2561566

1

0

1

1.0083732

1.0083732

0.0083732

1.112559

1.112559

0.5776615

19.453696

19.453696

14.34930

5.104393

0

0

1

-0.3617037

1

0

1

-0.2945485

-0.2945485

-1.2945485

5.422882

5.422882

4.3226736

22.147969

22.147969

12.00778

10.140192

1

1

1

-0.4995301

1

0

1

2.3817717

2.3817717

1.3817717

3.136195

3.136195

2.0409439

23.088961

23.088961

14.06501

9.023953

0

1

1

-1.5825305

1

0

0

-1.1021504

-0.1021504

-1.1021504

1.300471

1.950634

1.3004709

21.726949

25.643152

21.72695

3.916203

1

0

1

-0.7978039

1

0

1

-0.0289140

-0.0289140

-1.0289140

2.196055

2.196055

1.4959814

-6.400891

-6.400891

-11.52780

5.126911

1

0

1

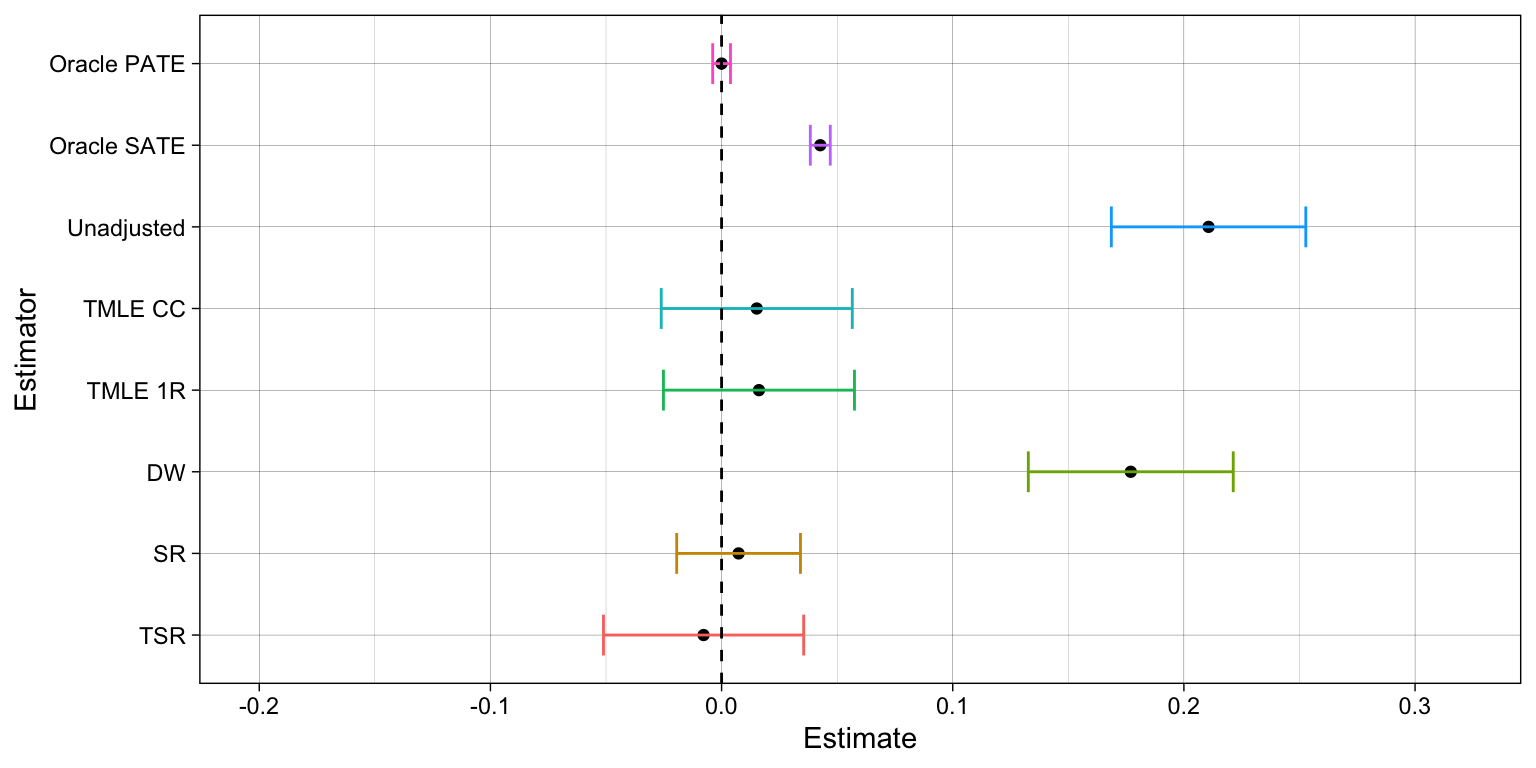

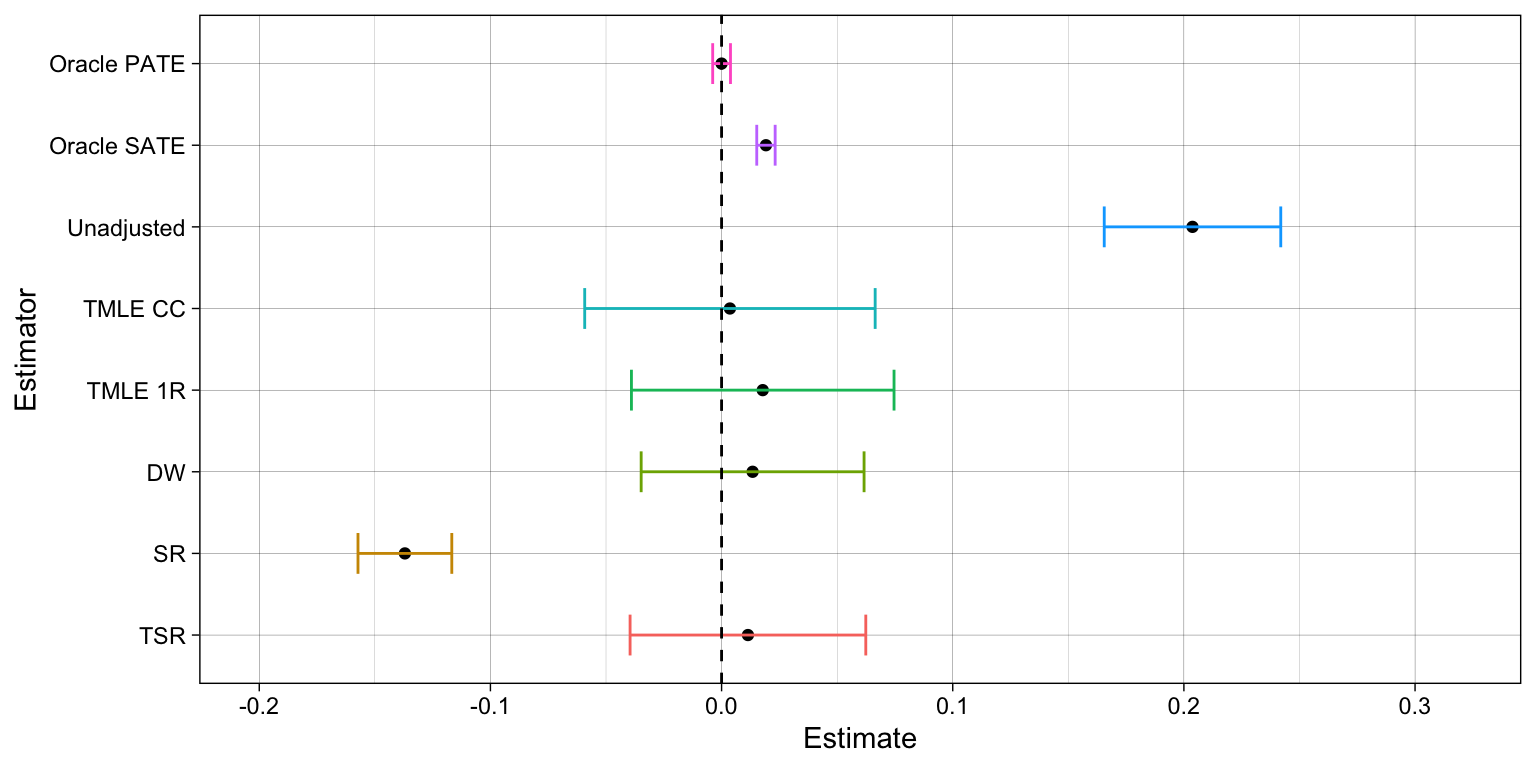

Estimators to compare

Table 1: estimators to be compared in simulations

Estimator

Method

Note

Oracle PATE sample-based

Average of ITE in the whole sample

Impossible to compute, we do not observe both counterfactuals nor missing outcome

Oracle SATE sample-based

Average of ITE in the selected sample

Impossible to compute, we do not observe both counterfactuals

Student’s t-test

Mean difference of observed outcomes treated vs control

It suffers from confounding and selection biases

TML CC

TMLE using only selected units: \(R_Y=1\)

It is not consistent in our DAG

TML 1R

TMLE adjusting only for pre-exposure \(W\)

It is not consistent in our DAG

Doubly weighted

Outcome difference weighted by propensity score and selection prob.

It is consistent in our DAG if models are correctly specified

Sequential regressions

Proposal 1

It is consistent in our DAG if models are correctly specified

Targeted SR

Proposal 2

It is consistent in our DAG with multiple robustness conditions

Super-learning procedure

Some estimators are produced under a super-learning scheme. They are based on weighted stacks of a library of base estimators: i) sample mean, ii) generalized linear model (GLM), and iii) spline regression model (earth package).

Code

# Learning algorithms employed to learn treatment/outcome mechanisms -----------# Mean modellrnr_me =make_learner(Lrnr_mean) # GLMlrnr_lm =make_learner(Lrnr_glm_fast)# Spline regressionlrnr_sp =make_learner(Lrnr_earth) # Meta-learners: to stack together predictions from the learners ---------------# Combine continuous predictions with non-negative least squaresmeta_C =make_learner(Lrnr_nnls) # Combine binary predictions with logit likelihood (augmented Lagrange optimizer)meta_B =make_learner(Lrnr_solnp, loss_function = loss_loglik_binomial, learner_function = metalearner_logistic_binomial) # Super-learners: learners + meta-learners together ----------------------------# Continuous super-learningsuper_C = Lrnr_sl$new(learners =list(lrnr_me, lrnr_lm, lrnr_sp), metalearner = meta_C)# Binary super-learningsuper_B = Lrnr_sl$new(learners =list(lrnr_me, lrnr_lm, lrnr_sp), metalearner = meta_B)# Super-learners put togethersuper_list =list(A = super_B,Y = super_C)

Generation of estimators

Code

################################################################################# TMLE-CC################################################################################tmlecc_estimator =function(Q1pre='',PSmis=''){if(Q1pre==''& PSmis==''){# Default TMLE package tmle.pret =tmle3(tmle_spec =tmle_ATE(1,0), # Targeting the ATEnode_list =list(W ='W', A ='A', Y ='Y'), # Variables involved data = full.data[sel,], # Data learner_list = super_list) # Super-learners # Save estimate and CI tmle.ptest =c(tmle.pret$summary$lower, tmle.pret$summary$upper, tmle.pret$summary$tmle_est) } elseif(Q1pre!=''& PSmis==''){# Model for treatment assignment train.A =make_sl3_Task(data = full.data[sel,], outcome ='A', covariates ='W') pred.A =make_sl3_Task(data = full.data, outcome ='A', covariates ='W') A_fit = super_B$train(task = train.A) full.data = full.data[, A_pre := A_fit$predict(task = pred.A)]# Model for Q1: MISSPECIFIED train.Q1 =lm(as.formula(Q1pre), data = full.data[sel,]) full.data = full.data[, Q1 :=predict(train.Q1, newdata = full.data)] %>% .[, clever.H1 := ((A/A_pre)-(1-A)/(1-A_pre))] # Define fluctuation model fluct.model.1=lm(Y ~-1+offset(Q1) + clever.H1, data=full.data[sel,])# Auxiliary data frame for prediction temp.dt =copy(full.data)# Using estimated fluctuation parameter, update Q1.1 temp.dt$A =1 full.data = full.data[, Q1.1:=predict(train.Q1, newdata = temp.dt)] %>% .[, up.Q1.1:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.1,clever.H1=(1/A_pre)))]# Using estimated fluctuation parameter, update Q1.0 temp.dt$A =0 full.data = full.data[, Q1.0:=predict(train.Q1, newdata = temp.dt)] %>% .[, up.Q1.0:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.0,clever.H1=(-1/(1-A_pre))))]# Compute the updated difference Q1.1 - Q1.0# Compute the observed value for up.Q1# Compute the value of the efficient influence function full.data = full.data[, delta.up.Q1 := up.Q1.1-up.Q1.0] %>% .[, up.Q1.A := A*up.Q1.1+ (1-A)*up.Q1.0] %>% .[, EIF := delta.up.Q1 + clever.H1*(Y - up.Q1.A)]# Using the EIF, compute the asymptotic error asymp.sd =sd(full.data[sel,EIF])/sqrt(nrow(full.data[sel,]))# Save estimate and CI tmle.ptest =c(mean(full.data[sel,delta.up.Q1])-qnorm(0.975)*asymp.sd,mean(full.data[sel,delta.up.Q1])+qnorm(0.975)*asymp.sd,mean(full.data[sel,delta.up.Q1])) }elseif(Q1pre==''& PSmis!=''){# Model for treatment assignment train.A =glm(as.formula(PSmis), full.data[sel,], family=binomial('logit')) full.data = full.data[, A_pre :=predict(train.A, type='response', newdata = full.data)]# Model for Q1 train.Q1 =make_sl3_Task(data = full.data[sel,], outcome ='Y', covariates =c('W','A')) Q1_fit = super_C$train(task = train.Q1)# Prediction task for Q1 pred.Q1 =make_sl3_Task(data = full.data, outcome ='Y', covariates =c('W','A')) full.data = full.data[, Q1 := Q1_fit$predict(task = pred.Q1)] %>% .[, clever.H1 := ((A/A_pre)-(1-A)/(1-A_pre))] # Define fluctuation model fluct.model.1=lm(Y ~-1+offset(Q1) + clever.H1, data=full.data[sel,])# Auxiliary data frame for prediction temp.dt =copy(full.data) temp.dt$A =1 pred.Q1 =make_sl3_Task(data = temp.dt, outcome ='Y', covariates =c('W','A')) full.data = full.data[, Q1.1:= Q1_fit$predict(task = pred.Q1)] %>% .[, up.Q1.1:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.1,clever.H1=(1/A_pre)))]# Using estimated fluctuation parameter, update Q1.0 temp.dt$A =0 pred.Q1 =make_sl3_Task(data = temp.dt, outcome ='Y', covariates =c('W','A')) full.data = full.data[, Q1.0:= Q1_fit$predict(task = pred.Q1)] %>% .[, up.Q1.0:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.0,clever.H1=(-1/(1-A_pre))))]# Compute the updated difference Q1.1 - Q1.0# Compute the observed value for up.Q1# Compute the value of the efficient influence function full.data = full.data[, delta.up.Q1 := up.Q1.1-up.Q1.0] %>% .[, up.Q1.A := A*up.Q1.1+ (1-A)*up.Q1.0] %>% .[, EIF := delta.up.Q1 + clever.H1*(Y - up.Q1.A)]# Using the EIF, compute the asymptotic error asymp.sd =sd(full.data[sel,EIF])/sqrt(nrow(full.data[sel,]))# Save estimate and CI tmle.ptest =c(mean(full.data[sel,delta.up.Q1])-qnorm(0.975)*asymp.sd,mean(full.data[sel,delta.up.Q1])+qnorm(0.975)*asymp.sd,mean(full.data[sel,delta.up.Q1])) }return(tmle.ptest)}################################################################################# DW################################################################################tmledw_estimator =function(Rpos='',PSmis=''){if(PSmis==''){# Model for treatment assignment train.A =make_sl3_Task(data = full.data, outcome ='A', covariates ='W') A_fit = super_B$train(task = train.A) full.data = full.data[, A_pre := A_fit$predict(task = train.A)] }else{# Model for treatment assignment train.A =glm(as.formula(PSmis), full.data, family=binomial('logit')) full.data = full.data[, A_pre :=predict(train.A, type='response')] }if(Rpos==''){# Model for missingness mechanism train.R =make_sl3_Task(data = full.data, outcome ='R0', covariates =c('W','A','M','Z')) R_fit = super_B$train(task = train.R) full.data = full.data[, R_pre := R_fit$predict(task = train.R)] }else{ train.R =glm(as.formula(Rpos), full.data, family=binomial('logit')) full.data = full.data[, R_pre :=predict(train.R, type='response')] } full.data = full.data[, DIW := (1/R_pre)*((A/A_pre)+(1-A)/(1-A_pre))] diw.mod =lm_robust(Y~A, full.data[sel,], weights = DIW)# Save estimate and CI diw.est =unname(c(diw.mod$conf.low[2], diw.mod$conf.high[2], diw.mod$coefficients[2]))return(diw.est)}################################################################################# SR################################################################################sr_estimator =function(Q1pos='',BS=30,Q2mis=''){if(Q1pos==''){# Model for Q1 train.Q1 =make_sl3_Task(data = full.data[sel,], outcome ='Y', covariates =c('W','A','M','Z')) Q1_fit = super_C$train(task = train.Q1)# Prediction task for Q1 pred.Q1 =make_sl3_Task(data = full.data, outcome ='Y', covariates =c('W','A','M','Z')) full.data = full.data[, Q1 := Q1_fit$predict(task = pred.Q1)] } else {# Model for Q1: MISSPECIFIED train.Q1 =lm(as.formula(Q1pos), data = full.data[sel,]) full.data = full.data[, Q1 :=predict(train.Q1, newdata = full.data)] }if(Q2mis==''){# Model for Q2.1 train.Q2.1=make_sl3_Task(data = full.data[A==1,], outcome ='Q1', covariates =c('W')) Q2.1_fit = super_C$train(task = train.Q2.1) pred.Q2.1=make_sl3_Task(data = full.data, outcome ='Q1', covariates =c('W')) full.data = full.data[, Q2.1:= Q2.1_fit$predict(task = pred.Q2.1)]# Model for Q2.0 train.Q2.0=make_sl3_Task(data = full.data[A==0,], outcome ='Q1', covariates =c('W')) Q2.0_fit = super_C$train(task = train.Q2.0) pred.Q2.0=make_sl3_Task(data = full.data, outcome ='Q1', covariates =c('W')) full.data = full.data[, Q2.0:= Q2.0_fit$predict(task = pred.Q2.0)] %>% .[, delta := full.data$Q2.1-full.data$Q2.0] }else {# Model for Q2 misspecified train.Q2 =lm(as.formula(Q2mis), full.data) full.data = full.data[, Q2.1:=predict(train.Q2, newdata=data.frame(W=full.data$W,A=1))] %>% .[, Q2.0:=predict(train.Q2, newdata=data.frame(W=full.data$W,A=0))] %>% .[, delta := full.data$Q2.1-full.data$Q2.0] }# Bootstrap procedure to compute the standard deviation bsamples =c()for(j in1:BS){# Boostraped data ind =sample(1:N,N,replace=T) bs.data =copy(full.data[ind,])if(Q1pos==''){# Model for Q1 train.bs.Q1 =make_sl3_Task(data = bs.data[sel,], outcome ='Y', covariates =c('W','A','M','Z')) bs.Q1_fit = super_C$train(task = train.bs.Q1)# Prediction task for Q1 pred.bs.Q1 =make_sl3_Task(data = bs.data, outcome ='Y', covariates =c('W','A','M','Z')) bs.data$Q1 = bs.Q1_fit$predict(task = pred.bs.Q1) }else {# Model for Q1: MISSPECIFIED train.bs.Q1 =lm(as.formula(Q1pos), data = bs.data[sel,]) bs.data$Q1 =predict(train.bs.Q1, newdata = bs.data) }if(Q2mis==''){# Model for Q2.1. train.bs.Q2.1=make_sl3_Task(data = bs.data[A==1,], outcome ='Q1', covariates =c('W')) bs.Q2.1_fit = super_C$train(task = train.bs.Q2.1) pred.bs.Q2.1=make_sl3_Task(data = bs.data, outcome ='Q1', covariates =c('W')) bs.data$Q2.1= bs.Q2.1_fit$predict(task = pred.bs.Q2.1)# Model for Q2.0 train.bs.Q2.0=make_sl3_Task(data = bs.data[A==0,], outcome ='Q1', covariates =c('W')) bsQ2.0_fit = super_C$train(task = train.bs.Q2.0) pred.bs.Q2.0=make_sl3_Task(data = bs.data, outcome ='Q1', covariates =c('W')) bs.data$Q2.0= Q2.0_fit$predict(task = pred.bs.Q2.0) }else {# Model for Q2 train.bs.Q2 =lm(as.formula(Q2mis), bs.data) full.data$Q2.1=predict(train.bs.Q2, newdata=data.frame(W=bs.data$W,A=1)) full.data$Q2.0=predict(train.bs.Q2, newdata=data.frame(W=bs.data$W,A=0)) }# Add predicted difference Q2.1 - Q2.0 to boostrap vessel bsamples =c(bsamples, mean(bs.data$Q2.1-bs.data$Q2.0)) }# Save estimate and CI nesreg.T =c(as.numeric(mean(full.data$delta) - (quantile(bsamples, 0.975)-quantile(bsamples, 0.025))/2),as.numeric(mean(full.data$delta) + (quantile(bsamples, 0.975)-quantile(bsamples, 0.025))/2),mean(full.data$delta))}################################################################################# TSR################################################################################tsr_estimator =function(Q1pos='',Q2mis=''){# STEP 1 ------------------if(Q1pos==''){# Model for Q1 train.Q1 =make_sl3_Task(data = full.data[sel,], outcome ='Y', covariates =c('W','A','M','Z')) Q1_fit = super_C$train(task = train.Q1)# Prediction task for Q1 pred.Q1 =make_sl3_Task(data = full.data, outcome ='Y', covariates =c('W','A','M','Z')) full.data = full.data[, Q1 := Q1_fit$predict(task = pred.Q1)] } else {# Model for Q1: MISSPECIFIED train.Q1 =lm(as.formula(Q1pos), data = full.data[sel,]) full.data = full.data[, Q1 :=predict(train.Q1, newdata = full.data)] }# Define clever variable full.data = full.data[, clever.H1 := (1/R_pre)*((A/A_pre)-(1-A)/(1-A_pre))] # Define fluctuation model fluct.model.1=lm(Y ~-1+offset(Q1) + clever.H1, data=full.data[sel,])# Auxiliary data frame for prediction temp.dt =copy(full.data)if(Q1pos==''){# Using estimated fluctuation parameter, update Q1.1 temp.dt$A =1 pred.Q1 =make_sl3_Task(data = temp.dt, outcome ='Y', covariates =c('W','A','M','Z')) full.data = full.data[, Q1.1:= Q1_fit$predict(task = pred.Q1)] %>% .[, up.Q1.1:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.1,clever.H1=(1/R_pre)*(1/A_pre)))]# Using estimated fluctuation parameter, update Q1.0 temp.dt$A =0 pred.Q1 =make_sl3_Task(data = temp.dt, outcome ='Y', covariates =c('W','A','M','Z')) full.data = full.data[, Q1.0:= Q1_fit$predict(task = pred.Q1)] %>% .[, up.Q1.0:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.0,clever.H1=(1/R_pre)*(-1/(1-A_pre))))] }else {# Using estimated fluctuation parameter, update Q1.1 temp.dt$A =1 full.data = full.data[, Q1.1:=predict(train.Q1, newdata = temp.dt)] %>% .[, up.Q1.1:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.1,clever.H1=(1/R_pre)*(1/A_pre)))]# Using estimated fluctuation parameter, update Q1.0 temp.dt$A =0 full.data = full.data[, Q1.0:=predict(train.Q1, newdata = temp.dt)] %>% .[, up.Q1.0:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.0,clever.H1=(1/R_pre)*(-1/(1-A_pre))))] }if(Q2mis==''){# Learn Q2.1 from up.Q1.1, using A=1 cases temp.dt =copy(full.data[A==1,]) train.Q2 =make_sl3_Task(data = temp.dt, outcome ='up.Q1.1', covariates =c('W')) Q2_fit = super_C$train(task = train.Q2) pred.Q2 =make_sl3_Task(data = full.data, outcome ='up.Q1.1', covariates =c('W')) full.data = full.data[, Q2.1:= Q2_fit$predict(task = pred.Q2)]# Learn Q2.0 from up.Q1.0, using A=0 cases temp.dt =copy(full.data[A==0,]) train.Q2 =make_sl3_Task(data = temp.dt, outcome ='up.Q1.0', covariates =c('W')) Q2_fit = super_C$train(task = train.Q2) pred.Q2 =make_sl3_Task(data = full.data, outcome ='up.Q1.0', covariates =c('W')) full.data = full.data[, Q2.0:= Q2_fit$predict(task = pred.Q2)]# STEP 2 ------------------# Compute the observed values for up.Q1 and Q2# Define clever variable full.data = full.data[, up.Q1.A := A*up.Q1.1+ (1-A)*up.Q1.0 ] %>% .[, Q2.A := A*Q2.1+ (1-A)*Q2.0 ] %>% .[, clever.H2 := ((A/A_pre)-(1-A)/(1-A_pre))] # Define fluctuation model fluct.model.2=lm(up.Q1.A ~-1+offset(Q2.A) + clever.H2, data=full.data)# Using estimated fluctuation parameter, update Q2.1 full.data = full.data[, up.Q2.1:=predict(fluct.model.2, newdata =data.frame(Q2.A=full.data$Q2.1,clever.H2=1/A_pre))] %>% .[, up.Q2.0:=predict(fluct.model.2,newdata =data.frame(Q2.A=full.data$Q2.0,clever.H2=-1/(1-A_pre)))] }else { full.data = full.data[, up.Q1.A := A*up.Q1.1+ (1-A)*up.Q1.0 ] Q2mismod =gsub("Q1", "up.Q1.A", Q2mis) train.Q2 =lm(as.formula(Q2mismod), full.data) full.data = full.data[, Q2.1:=predict(train.Q2, newdata=data.frame(W=full.data$W,A=1))] %>% .[, Q2.0:=predict(train.Q2, newdata=data.frame(W=full.data$W,A=0))]# STEP 2 ------------------# Compute the observed values for up.Q1 and Q2# Define clever variable full.data = full.data[, Q2.A := A*Q2.1+ (1-A)*Q2.0 ] %>% .[, clever.H2 := ((A/A_pre)-(1-A)/(1-A_pre))] # Define fluctuation model fluct.model.2=lm(up.Q1.A ~-1+offset(Q2.A) + clever.H2, data=full.data)# Using estimated fluctuation parameter, update Q2.1 full.data = full.data[, up.Q2.1:=predict(fluct.model.2, newdata =data.frame(Q2.A=full.data$Q2.1,clever.H2=1/A_pre))] %>% .[, up.Q2.0:=predict(fluct.model.2, newdata =data.frame(Q2.A=full.data$Q2.0,clever.H2=-1/(1-A_pre)))] }# Compute the updated difference Q2.1 - Q2.0# Compute the observed value for up.Q2# Compute the value of the efficient influence function full.data = full.data[, delta.up.Q2 := up.Q2.1-up.Q2.0] %>% .[, up.Q2.A := A*up.Q2.1+ (1-A)*up.Q2.0] %>% .[, EIF := delta.up.Q2 + clever.H2*(up.Q1.A - up.Q2.A) + clever.H1*(Y - up.Q1.A)*R0]# Using the EIF, compute the asymptotic error asymp.sd =sd(full.data$EIF)/sqrt(N)# Save estimate and CI tmle.2step =c(mean(full.data$delta.up.Q2)-qnorm(0.975)*asymp.sd,mean(full.data$delta.up.Q2)+qnorm(0.975)*asymp.sd,mean(full.data$delta.up.Q2))return(tmle.2step)}################################################################################# TMLE-1R################################################################################tmle1r_estimator =function(Q1pre='',Rpre=''){# Update R-predictionsif(Rpre==''){# Model for missingness mechanism train.R =make_sl3_Task(data = full.data, outcome ='R0', covariates =c('W','A')) R_fit = super_B$train(task = train.R) full.data = full.data[, R_pre := R_fit$predict(task = train.R)] }else{ train.R =glm(as.formula(Rpre), full.data, family=binomial('logit')) full.data = full.data[, R_pre :=predict(train.R, type='response')] }# Update Q-predictionsif(Q1pre==''){# Model for Q1 train.Q1 =make_sl3_Task(data = full.data[sel,], outcome ='Y', covariates =c('W','A')) Q1_fit = super_C$train(task = train.Q1)# Prediction task for Q1 pred.Q1 =make_sl3_Task(data = full.data, outcome ='Y', covariates =c('W','A')) full.data = full.data[, Q1 := Q1_fit$predict(task = pred.Q1)] }else {# Model for Q1: MISSPECIFIED train.Q1 =lm(as.formula(Q1pre), data = full.data[sel,]) full.data = full.data[, Q1 :=predict(train.Q1, newdata = full.data)] }# Define clever variable full.data = full.data[, clever.H1 := (1/R_pre)*((A/A_pre)-(1-A)/(1-A_pre))] # Define fluctuation model fluct.model.1=lm(Y ~-1+offset(Q1) + clever.H1, data=full.data[sel,])# Auxiliary data frame for prediction temp.dt =copy(full.data)if(Q1pre==''){# Using estimated fluctuation parameter, update Q1.1 temp.dt$A =1 pred.Q1 =make_sl3_Task(data = temp.dt, outcome ='Y', covariates =c('W','A')) full.data = full.data[, Q1.1:= Q1_fit$predict(task = pred.Q1)] %>% .[, up.Q1.1:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.1,clever.H1=(1/R_pre)*(1/A_pre)))]# Using estimated fluctuation parameter, update Q1.0 temp.dt$A =0 pred.Q1 =make_sl3_Task(data = temp.dt, outcome ='Y', covariates =c('W','A')) full.data = full.data[, Q1.0:= Q1_fit$predict(task = pred.Q1)] %>% .[, up.Q1.0:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.0,clever.H1=(1/R_pre)*(-1/(1-A_pre))))] }else{# Using estimated fluctuation parameter, update Q1.1 temp.dt$A =1 full.data = full.data[, Q1.1:=predict(train.Q1, newdata = temp.dt)] %>% .[, up.Q1.1:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.1,clever.H1=(1/R_pre)*(1/A_pre)))]# Using estimated fluctuation parameter, update Q1.0 temp.dt$A =0 full.data = full.data[, Q1.0:=predict(train.Q1, newdata = temp.dt)] %>% .[, up.Q1.0:=predict(fluct.model.1, newdata =data.frame(Q1=full.data$Q1.0,clever.H1=(1/R_pre)*(-1/(1-A_pre))))] }# Compute the updated difference Q1.1 - Q1.0# Compute the observed value for up.Q1# Compute the value of the efficient influence function full.data = full.data[, delta.up.Q1 := up.Q1.1-up.Q1.0] %>% .[, up.Q1.A := A*up.Q1.1+ (1-A)*up.Q1.0] %>% .[, EIF := delta.up.Q1 + clever.H1*(Y - up.Q1.A)*R0]# Using the EIF, compute the asymptotic error asymp.sd =sd(full.data$EIF)/sqrt(N)# Save estimate and CI tmle.1step =c(mean(full.data$delta.up.Q1)-qnorm(0.975)*asymp.sd,mean(full.data$delta.up.Q1)+qnorm(0.975)*asymp.sd,mean(full.data$delta.up.Q1))return(tmle.1step)}

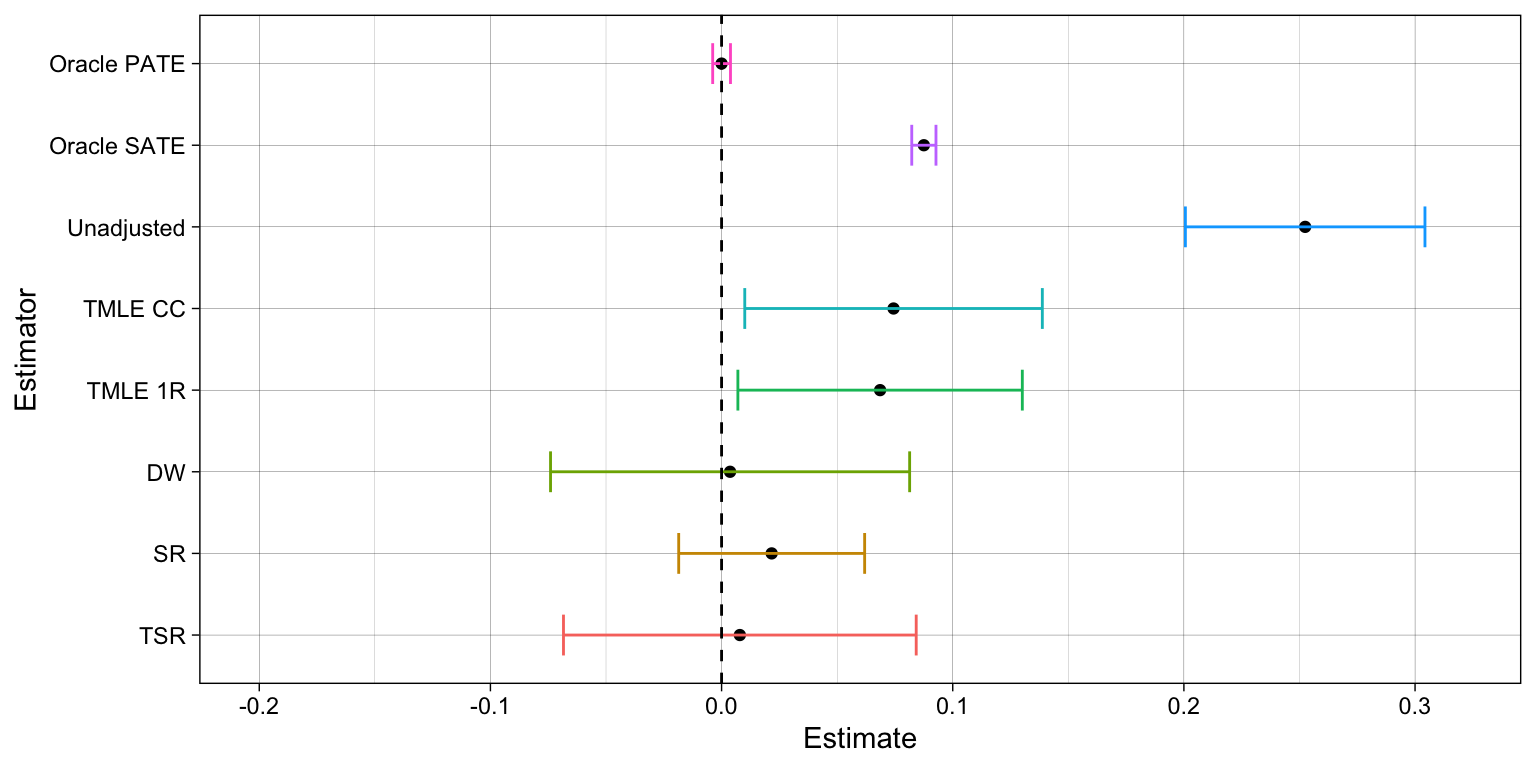

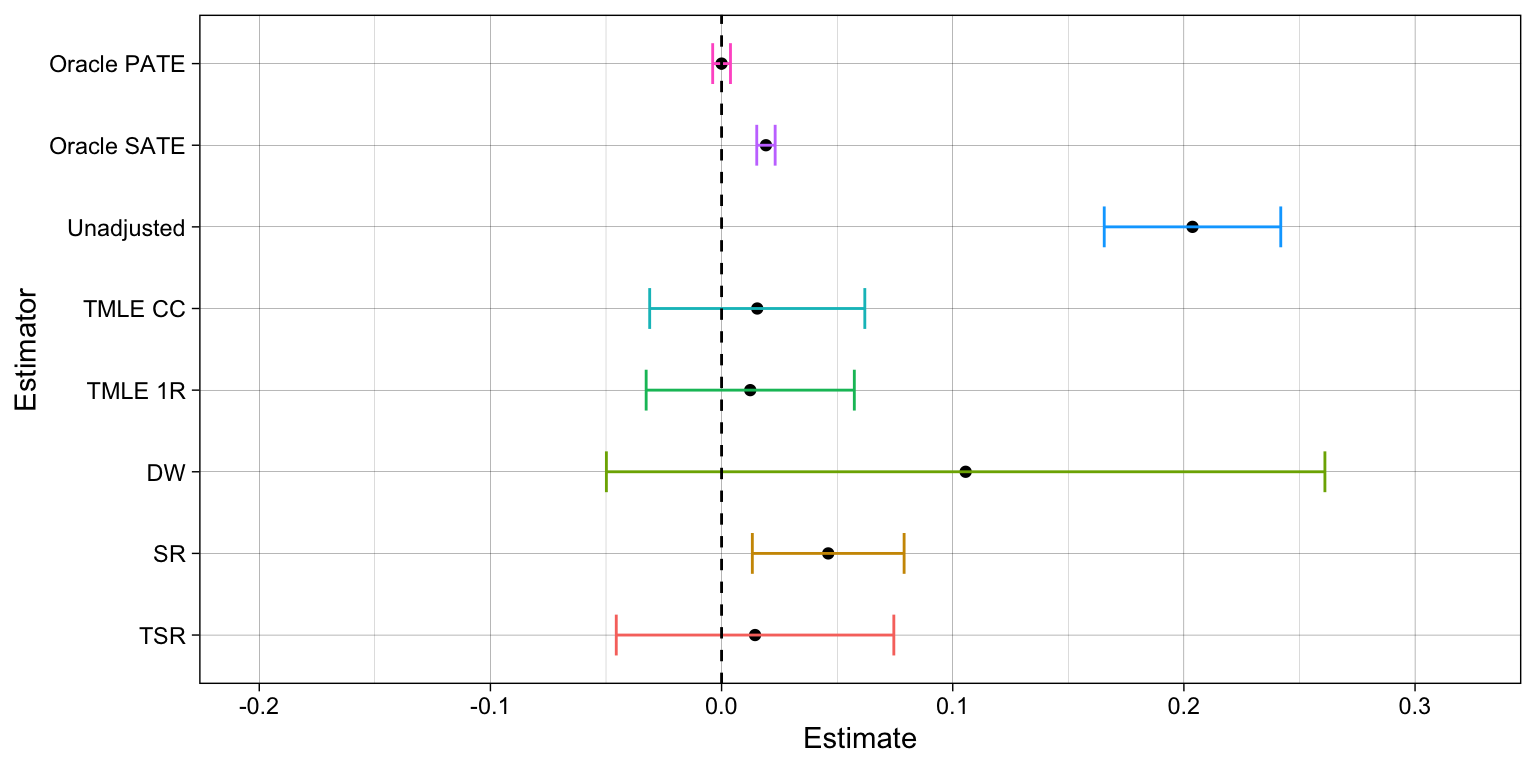

Case 1: severe missingness/selection and no misspecification

Code

# SELECTION MECHANISMfull.data$R0 =1full.data$R0 = full.data$R1#-------------------------------------------------------------------------------# Estimator A: Oracle PATE -----------------------------------------------------oracle.ttest =t.test(full.data$ITE)pate =unname(c(oracle.ttest$conf.int[1], oracle.ttest$conf.int[2], oracle.ttest$estimate))#-------------------------------------------------------------------------------# Estimator B: Oracle SATE -----------------------------------------------------sel = (full.data$R0==1)oracle.ttest =t.test(full.data[sel,ITE])sate =unname(c(oracle.ttest$conf.int[1], oracle.ttest$conf.int[2], oracle.ttest$estimate))#-------------------------------------------------------------------------------# Estimator 1: Unadjusted t-test -----------------------------------------------unadj.mod =lm_robust(Y~A,full.data[sel,])# Save estimate and CIunadj.est =unname(c(unadj.mod$conf.low[2], unadj.mod$conf.high[2], unadj.mod$coefficients[2]))#-------------------------------------------------------------------------------# Estimator 2: TMLE CC ---------------------------------------------------------tmle.ptest =tmlecc_estimator()#-------------------------------------------------------------------------------# Estimator 3: Doubly-inverse weighted estimator -------------------------------diw.est =tmledw_estimator()#-------------------------------------------------------------------------------# Estimator 4: Nested regressions, T-learner -----------------------------------nesreg.T =sr_estimator()#-------------------------------------------------------------------------------# Estimator 5: 2-step TMLE ----------------------------------------------------tmle.2step =tsr_estimator()#-------------------------------------------------------------------------------# Estimator 6: pre-exp TMLE ---------------------------------------------------tmle.1step =tmle1r_estimator()#-------------------------------------------------------------------------------# PUT ALL TOGETHER -------------------------------------------------------------estimators =data.table(rbind(pate,sate,unadj.est,tmle.ptest, tmle.1step,diw.est,nesreg.T,tmle.2step))colnames(estimators) =c('lower','upper','point.est')estimators$type =c('Oracle PATE','Oracle SATE',"Unadjusted",'TMLE CC','TMLE 1R','DW','SR','TSR')estimators$type =factor(estimators$type,levels =rev(estimators$type))# Bias in scale of percentage points over the outcome's standard deviationusd =sd(full.data$Y)bia =as.numeric(estimators[1,3])estimators = estimators[,lower := (lower-bia)/usd] %>% .[,upper := (upper-bia)/usd] %>% .[,point.est := (point.est-bia)/usd] # Estimate and CI plotggplot(estimators, aes(y=type, x=point.est, group=type)) +geom_point(position=position_dodge(0.78)) +geom_errorbar(aes(xmin=lower, xmax=upper, color=type),width=0.5, position=position_dodge(0.78)) +guides(color=FALSE) +labs(x='Estimate',y='Estimator') +theme_linedraw() +xlim(c(-0.2,0.32)) +geom_vline(xintercept =0, linetype="dashed")

SR estimator provides the best alternative under the assumption of correct model specifications. It can consistently recover the ATE from confounding and selection bias (under conditional ignorability and recoverability conditions). It casts a narrower confidence interval relative to the DW and TSR estimators. Yet, it requires a bootstrap procedure to compute standard errors, which might be costly in complex models/datasets, and it fails to be consistent when one the outcome models is not correctly specified.

TSR estimator is less efficient than SR, producing wider confidence intervals, but it is more efficient than the DW estimator. Moreover, it remains consistent even when some of the outcome models are not correctly specified, provided the treatment assignment and missingness mechanisms are both correct.

van der Laan, M. J., and S. Rose. 2011. Targeted Learning: Causal Inference for Observational and Experimental Data. Springer Series in Statistics. Springer New York. https://books.google.no/books?id=RGnSX5aCAgQC.